TL;DR

- Inventory discrepancy means your system records don’t match physical stock. Most companies think they have 95% accuracy but actually operate at 65-75%. That gap is ghost inventory.

- Root causes are systematic: data entry errors, receiving failures, misplacement, unlogged consumption, yield variance in manufacturing.

- Discrepancies cause production halts from missing materials, permanent customer loss, and working capital gets trapped.

- Process fixes deliver most improvement at minimal cost. Standardize receiving with scanning, implement cycle counting for high-value items, assign one person accountability, document all procedures.

- You can self-diagnose using 12 red flags: month-end surprises, can’t find items, accuracy below 85%, team uses backup counts, customer complaints, production halts. If 4+ are true you have a problem. If 8+ it’s a crisis.

Your System Says You Have It. Your Warehouse Doesn’t.

It was a Tuesday morning when the warehouse manager’s call came in. The manufacturing plant had a problem.

The system showed 47 bearing assemblies in stock. The customer order was ready to fulfill. Production was scheduled. Everything looked fine on the spreadsheet.

But when the warehouse team went to pick the bearings, they found 3 units. Not 47. Nobody knew where the other 44 units went.

The production line stopped. The customer shipment was delayed by two weeks. And somewhere in the financial records, ₹15 lakhs worth of inventory simply vanished, at least from the perspective of actual cash in hand.

This wasn’t a one-time incident at one facility. It’s systematic. It’s happening in warehouses across India right now. And it’s costing manufacturing businesses far more than they realize.

What You’re Actually Dealing With

Inventory discrepancy sounds like a technical warehouse problem. It’s not. It’s a cash flow crisis wearing a data management disguise.

Here’s what it actually means: Your system says you have ₹50 lakhs in inventory. Your warehouse physically has ₹35 lakhs. That ₹15 lakh gap, the ghost inventory, is cash you’ve already paid for but can’t use.

Ghost inventory is when your system says an item is in stock, but it isn’t. It was stolen, damaged, lost, or misplaced.

Inventory shrinkage is the physical loss of inventory. 65.5% of shrinkage comes from theft, the rest from damage and waste.

Inventory discrepancy is the broader problem, system records don’t match physical reality. It includes both ghost inventory and shrinkage, plus data entry errors, receiving mistakes, and unlogged movements.

When you conflate all three, you fix the wrong problem. You implement theft prevention when your real issue is data entry errors. You buy a warehouse management system when you need better receiving procedures. You chase symptoms instead of solving the disease.

Why This Matters to Your Cash Flow (Right Now)

Stop thinking about this as an operational problem. Think about it as a liquidity problem.

When you discover you have ₹15 lakhs in ghost inventory, you don’t have ₹15 lakhs available for operations. You’ve paid your suppliers. The cash is gone. But the inventory doesn’t exist to sell, so that cash never comes back.

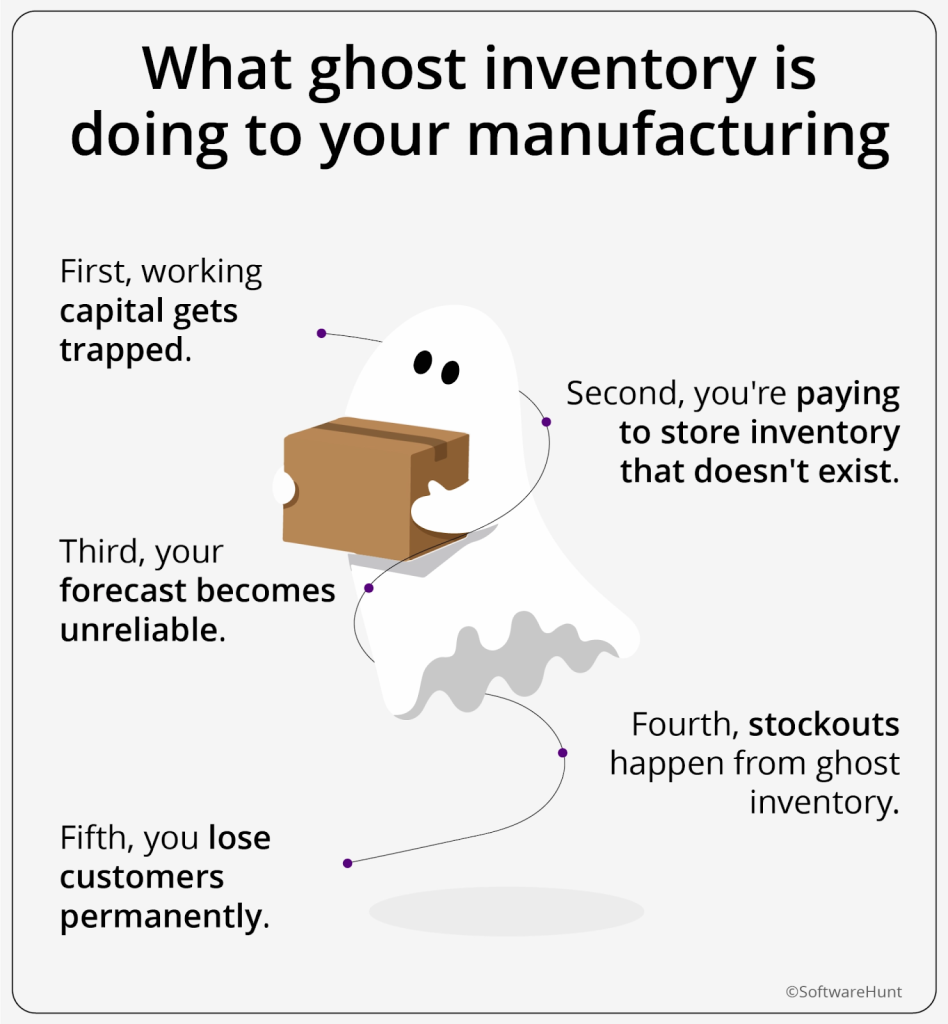

Here’s the cascade:

First, working capital gets trapped.

You operate with a certain amount of cash to fund day-to-day operations. When ghost inventory inflates your recorded inventory value, you think you have more assets than you do. So you make decisions assuming that capital is available. It isn’t. You hit a cash crunch you didn’t expect.

Second, you’re paying to store inventory that doesn’t exist.

Ghost inventory still consumes warehouse space in your mind. You’re paying rent, utilities, insurance, and handling costs for goods that exist only in your system. For every ₹1 million in ghost inventory, you’re spending ₹180,000 to ₹240,000 annually in carrying costs, money for nothing.

Third, your forecast becomes unreliable.

Your demand forecast is built on historical sales data. But if your inventory records are wrong, your sales data is wrong. You think you sold 100 units last month when you actually sold 60. So you forecast demand at 100 this month. You over-order. Now you have more ghost inventory. The cycle gets worse.

Fourth, stockouts happen from ghost inventory.

Your system says you have material. You schedule production. You start the line. The material isn’t actually there, it’s ghost inventory. The line stops. A production line stoppage costs ₹50,000+ per hour. One line stop per month from ghost inventory means ₹6 lakhs+ in unplanned downtime annually.

Fifth, you lose customers permanently.

When customers experience stockouts caused by ghost inventory, 33% of them switch to a competitor. They don’t come back. One permanent customer loss might cost you ₹5-10 lakhs in lifetime value.

Where Discrepancies Actually Come From

Most manufacturers think the problem is either “people aren’t paying attention” or “our warehouse system is bad.” Usually it’s neither. It’s systematic.

Data entry errors are the biggest culprit. When a receiving clerk enters shipment data manually, they transpose numbers. They enter “01” instead of “10.” They scan the wrong SKU. A batch of 100 units gets recorded as 50. Nobody catches it because monthly reconciliation is perfunctory.

Receiving failures come next. The supplier sends 95 units. The purchase order says 100. Instead of counting, the receiving team assumes the supplier got it right. They log 100 in the system. Now you have a ₹5 lakh discrepancy from day one.

Misplacement is where ghost inventory hides best. An item arrives but gets stored in the wrong location. The system thinks it’s in Bin A. It’s actually in Bin D. When you need it, you can’t find it. So you order another unit (paying 3x for expedited freight). Now you have two units—one ghost, one real—taking up space.

Unlogged consumption is especially common in manufacturing. Your production team consumes material but doesn’t log it out of inventory. The system still shows the material exists. So the next scheduled production run plans to use material that was already consumed. Ghost inventory.

Yield variance creates confusion in manufacturing specifically. You input 100 units of raw material into production. You get 85 usable finished units (15 units lost to defects and waste). If this isn’t tracked and logged properly, the system thinks you have 85 units of finished goods and still has the 100 units of raw material. Your inventory balance sheet is fictitious.

Supplier errors and returns pile on top. A supplier sends damaged goods. You don’t immediately record it as damage. It sits on the shelf as “good inventory.” Later, when you discover it’s damaged, nobody logs the adjustment. Ghost inventory.

System glitches and integration gaps are the final piece. Your Tally system records a purchase. Your warehouse management system doesn’t sync. Your production system thinks material is available but it isn’t allocated. Three systems, three versions of truth.

The research is clear: 0.94% of warehouses have a measurable discrepancy rate. For a ₹50 lakh inventory, that’s ₹4.7 lakhs unaccounted for. But 52.85% of products have inaccuracies when you actually count them.

The Cost Breakdown (What This Actually Costs You)

Let me show you the math for a typical ₹2 crore manufacturer:

Revenue loss from stockouts and ghost inventory: ₹4 lakhs. When customers can’t get items they expect to buy, 33% switch permanently. Lost customers mean lost revenue.

Carrying costs on ghost inventory: ₹3.6 lakhs annually. On ₹15 lakhs of ghost stock (30% of your ₹50 lakh inventory), you’re paying 24% in annual carrying costs – storage, utilities, insurance, handling.

Working capital financing costs: ₹1.8 lakhs annually. If you need to finance the ghost inventory at 12% interest, that’s ₹1.8 lakhs per year just to have money tied up in inventory you can’t sell.

Write-offs from obsolete ghost inventory: ₹1 lakh. Ghost inventory often becomes unsellable – seasonal goods marked down heavily, or items that expire before you realize you have them.

Labor waste on manual reconciliation: ₹50,000. Your finance team spends 1-2 weeks per month reconciling inventory discrepancies at month-end close.

Emergency expediting costs: ₹9 lakhs. To compensate for inventory visibility problems, you expedite shipments regularly (paying 3x normal freight), or emergency-order from suppliers at premium prices.

Production downtime: ₹6 lakhs. One unplanned production halt per month due to ghost inventory (thinking material is available when it isn’t).

Total annual impact: ₹25.45 lakhs. For a ₹2 crore business with a 10% net margin (₹20 lakhs profit), this represents 127% of your annual profit being lost to ghost inventory.

We’re SoftwareHunt. Our team sits with manufacturing owners to understand your operational leaks and growth challenges. We go beyond platform listings to help you find the right solution at no cost to you.

Email an advisor for a quick fit-check write to us at connect@softwarehunt.com

Why Manufacturers Are Especially Vulnerable

Manufacturing creates more points where discrepancies hide than any other business type.

A bill of materials can have 20-50+ line items. Each component is a point where discrepancy can be introduced. Raw materials come in, get converted to work-in-progress (WIP), then finish as completed goods. At each stage, tracking gets sloppier.

Work-in-progress is the blind spot. Unlike warehouse inventory which is organized in bins, WIP is scattered across your production floor. It’s on lathes, in quality inspection areas, between production stations, in staging areas. Nobody has a real-time view of where WIP actually is. So when you do a physical count, invariably the system doesn’t match reality. And WIP inventory has 6-9x more impact on your profitability than finished goods. So getting WIP wrong is catastrophic.

Yield variance creates phantom assets. Manufacturing accepts that some input becomes waste. You input 100 units, you get 85 usable units. That 15-unit loss needs to be tracked. If it isn’t logged properly, your system shows both the 100 units of input AND the 85 units of output—phantom assets that don’t exist.

Tally integration is a nightmare. Most mid-sized Indian manufacturers use Tally for accounting. Tally records a purchase (Dr. Inventory, Cr. Cash). But production consumes the material without logging it. Month-end, finance discovers the discrepancy. By then, multiple decisions have been made based on wrong data.

Erratic orders kill supplier relationships. Because your inventory data is unreliable, you over-order to compensate. Your orders become erratic—100 units one month, 50 the next, 300 the next. Your supplier can’t plan. They deprioritize you. Lead times increase. You panic-order bigger amounts. The bullwhip effect multiplies discrepancies.

How You Know You Have This Problem

You don’t need a consultant to diagnose this. Count how many of these are true for your business:

Red Flag 1: Physical inventory count doesn’t match system records more than 5-10% of the time.

Red Flag 2: Month-end inventory adjustments are always ₹2-5 lakhs (the “reconciliation surprise”).

Red Flag 3: Your warehouse can’t locate items the system says are in stock at least once a month.

Red Flag 4: Your actual inventory accuracy is below 85% (most companies think they’re at 95%, but when tested, they’re at 65-75%).

Red Flag 5: Your team keeps “backup” counts on paper because they don’t trust the system.

Red Flag 6: Customers regularly call to say “we thought you had this in stock.”

Red Flag 7: Carrying costs are rising even though inventory volume hasn’t increased proportionally.

Red Flag 8: Write-offs are increasing year-over-year.

Red Flag 9: Your warehouse staff spend 1+ hour per day searching for or verifying inventory.

Red Flag 10: Suppliers complain that your orders are “all over the place” and unpredictable.

Red Flag 11: Finance takes 1-2 extra weeks to close the month because of inventory reconciliation.

Red Flag 12: Production halts from “missing materials” happen more than once per month.

If 4+ of these are true, you have a discrepancy problem. If 8+, it’s a crisis.

Why Nobody Sees This Coming

The reason ghost inventory is so dangerous is that it’s invisible until it’s massive.

It doesn’t show up as a separate line item on your P&L. It’s scattered across COGS (shrinkage losses), variance accounts (month-end adjustments), and “Other expenses” (expediting fees). Nobody adds it up. You think you have a 10% net margin when you actually have 5%.

You only measure inventory accuracy annually or at quarterly physical counts. But ghost inventory happens daily. One unit gets damaged today. Another gets stolen tomorrow. A data entry error happens Thursday. By month-end, when you do the count, the discrepancy is so large you can’t trace it back to the root cause. You just adjust the balance sheet.

Operations and finance don’t communicate. The warehouse knows items are missing. Finance knows costs are higher. Neither group realizes they’re describing the same problem. Warehouse says “we think supplier quality is bad.” Finance says “demand variance is killing us.” Both miss the root cause: inventory data is wrong.

You normalize the problem. “Oh, we’ve always had variances at month-end.” “This is just how manufacturing works.” No. This is how poorly-managed manufacturing works. Better operators achieve 95%+ accuracy with no surprises.

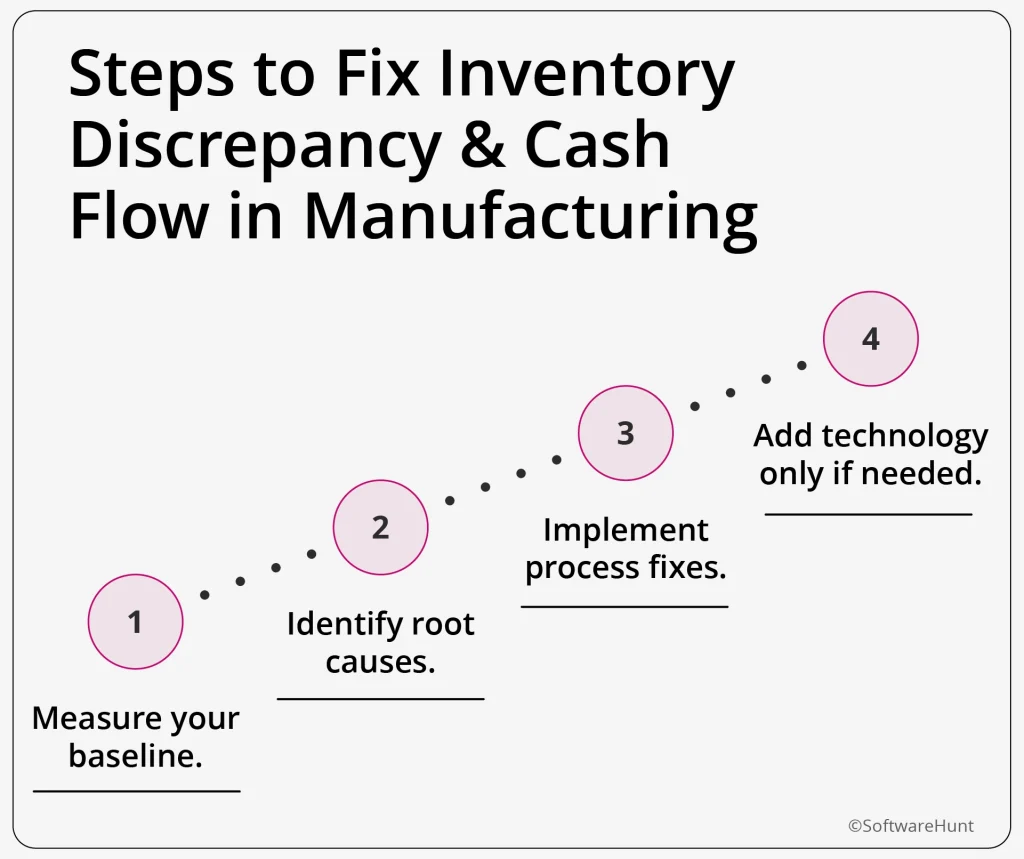

How to Actually Fix This

Don’t start with technology. Start with process.

Step 1: Measure your baseline.

Do a full physical count. Compare to system records. Calculate actual accuracy. Document discrepancies. Where are they concentrated? Receiving? Storage? Production? Cost: Labor only. Time: 1-2 weeks.

Step 2: Identify root causes.

For each major discrepancy, ask why. Data entry error? Receiving mistake? Theft? Misplacement? Unlogged consumption? Don’t assume – investigate. Then categorize by root cause.

Step 3: Implement process fixes.

This is where 80% of improvement happens, at minimal cost.

- Standardize receiving: Every item scanned against the purchase order. Compare quantity to packing slip. Flag discrepancies immediately.

- Implement cycle counting: High-value items counted weekly. Medium-value monthly. Low-value quarterly. Investigate discrepancies same day.

- Assign ownership: One person is accountable for inventory accuracy. Weekly accuracy reporting. Monthly trend analysis.

- Document procedures: No ad-hoc methods. Every process documented and trained.

Cost: ₹0-₹50,000. Improvement: Accuracy increases 10-20 percentage points in 3 months.

Step 4: Add technology only if needed.

If process improvements get you to 90%+ accuracy, stop, keep doing what works.

If stuck at 85-90%, evaluate whether technology helps. That evaluation is consultative, we assess YOUR specific situation at no cost.

Most discover 80% improvement happens with just process discipline.

Your 30/90/365 Day Roadmap

Days 1-30: Diagnostic phase. Physical count of high-value items. System comparison. Root cause analysis for top discrepancies. Document findings. Cost: Labor only. Outcome: You know exactly what’s broken and why.

Month 2-4: Process implementation. Start cycle counting. Standardize receiving. Assign accountability. Weekly accuracy reporting. Expected improvement: +15% accuracy. Cost: ₹0-₹20,000.

Month 5-12: Optimization & technology. If accuracy >90%, you’re done optimizing. Monthly accuracy reviews. Trend analysis. Target: 95%+ accuracy. Total annual financial impact: ₹15-33 lakhs in cost avoidance.

The Real Message

You’re not going to eliminate ghost inventory entirely. But you can go from 25-35% of inventory records being inaccurate to 95%+ being accurate. That difference is ₹15-25 lakhs in annual cash flow.

That’s not theoretical. That’s real cash. That’s working capital freed up. That’s avoiding emergency freight charges. That’s preventing production halts. That’s customers you keep instead of losing.

The first step isn’t buying a system. The first step is admitting the problem exists and measuring it.

Do a physical count of your high-value items this week. Compare to your system. See what you find.

Most manufacturers will be shocked.

We’re SoftwareHunt. We work with manufacturing owners running on Tally, Excel, and lean teams to understand your operational leaks and growth challenges. Our team is happy to connect with you, understand your personal pain points, operational leaks and growth challenges and go beyond platform listings/information to help find the right solution for you.

We’ll help you translate symptoms into clear financial insight and show you where to focus first – at no cost to you.

To email an advisor for a quick fit-check write to us at connect@softwarehunt.com.