Key Takeaways

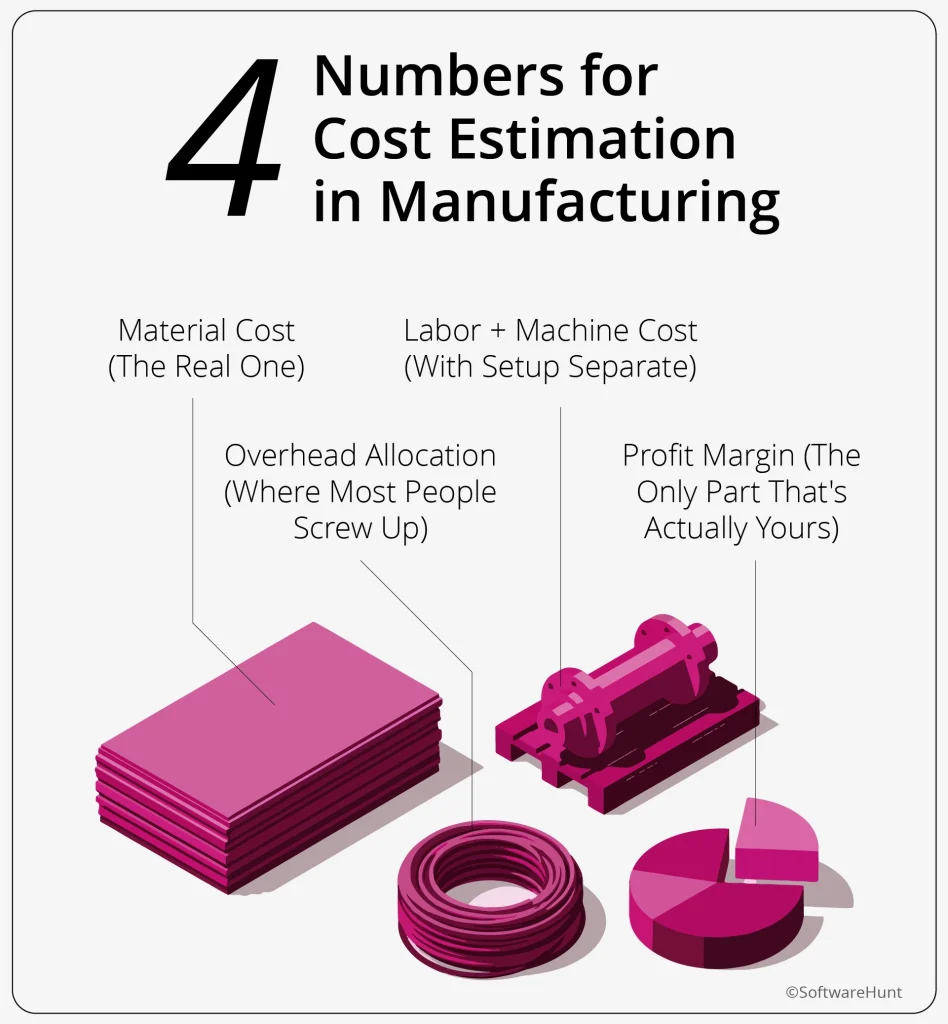

- Manufacturing cost has 4 numbers: material with measured scrap, labor plus machine with setup separate, overhead by complexity, profit on total cost.

- Problem: Material plus 60% markup covers everything. It doesn’t. That markup disappears into labor, overhead, scrap, and setup.

- Money hides in unmeasured scrap, uncounted setup time, wrong overhead allocation, stale pricing.

- Fix: Four weeks. Measure scrap. Track time. Calculate overhead. Then thirty minutes weekly.

It’s 4 PM at Kumar Chai Center near Pune’s industrial belt. Vikram Mehta, 42, owns a sheet metal fabrication unit. He’s staring at his phone, Excel open, showing a ₹5.2 lakh order that somehow lost ₹82,000.

He mutters something under his breath.

Anjali Rathod runs a CNC components shop three units down. She sees his expression.

Anjali: Bad order?

Vikram: The worst. Quoted ₹5.2 lakhs. Client paid. We delivered. Now I’m calculating actual costs… lost ₹82K.

Anjali: How did you quote it?

Vikram: Material cost plus 60% markup. Standard.

Anjali: [Sits down] Arre, that’s not a method. That’s a prayer.

What Anjali learned and what Vikram is about is that manufacturing cost calculation isn’t complicated. Most SME manufacturers in India skip real product costing and wonder why margins vanish on complex jobs.

This conversation changed how Vikram thinks about manufacturing costs. Not because Anjali had magical software or expensive consultants. She’d made the same mistake, lost ₹1.2 lakhs on a single order two years ago.

What she figured out is what most SME manufacturers miss: Manufacturing cost estimation isn’t about fancy formulas. It’s about knowing four numbers properly.

Why Material + Markup Fails Every Time

Vikram’s method is common. Buy material for ₹3.25 lakhs. Add 60% markup. Quote ₹5.2 lakhs. Done.

This is the most common manufacturing cost estimation mistake across tier 2/3 Indian factories. The markup feels like a buffer. It’s not. It’s a guess dressed as strategy.

But 60% was supposed to cover everything: labor, machine time, electricity, overheads, scrap, setup time, finishing, inspection, AND profit.

That never works on complex jobs.

Vikram: So what do you do?

Anjali: I calculate four numbers separately. Material. Labor plus machine. Overhead. Then add profit.

Vikram: Sounds like a lot of tracking.

Anjali: It’s 30 minutes once a week after you set it up. But it shows you where money actually goes.

She pulls out her phone. Shows him a recent job: automotive brackets, 500 units.

The Four Numbers That Actually Matter

Number One: Material Cost (The Real One)

Anjali: How much material did you buy for that ₹5.2L order?

Vikram: ₹3.25 lakhs. Steel sheets, fasteners, some specialty coating.

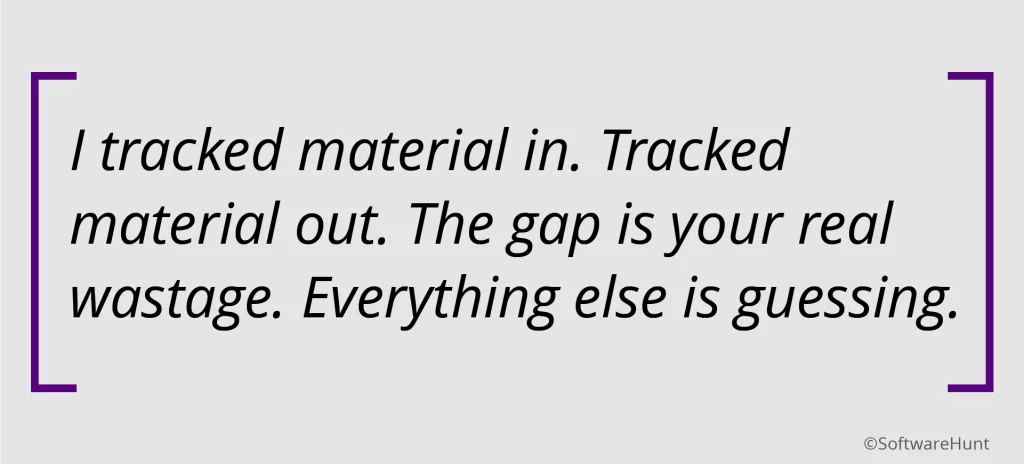

Anjali: And how much became scrap?

Vikram: [Pause] I don’t… track that separately.

This is where money disappears.

Anjali discovered this the hard way: manufacturers usually underestimate scrap. She was assuming 5% based on industry averages. Reality: 12.5% on her actual production. For Vikram’s order, that’s ₹32,500-48,750 missing from his estimate.

This is why accurate material cost tracking matters. Not estimates. Not industry averages. Your actual scrap percentage, measured monthly, is the foundation of all manufacturing cost calculation.

Anjali’s method:

She tracks three things:

- Raw material purchased: What she paid suppliers

- Scrap/wastage: What didn’t make it into finished products

- Transportation and handling: Freight, unloading, storage

For her 500-unit bracket job:

- Raw material: ₹38,000

- Scrap (12%): ₹4,560

- Transport/handling: ₹2,440

- Total material cost: ₹45,000

Vikram: Wait. How do you know your scrap rate?

Anjali: I compared what we bought monthly to what we shipped. Took 30 minutes. We buy ₹8 lakhs material. Ship products worth ₹7 lakhs material. That’s ₹1 lakh scrap. About 12.5%.

She used to assume 5%. Reality was 12%. Every quote was under-costed by 7%.

Number Two: Labor + Machine Cost (With Setup Separate)

Vikram: Labor is simple. I pay my guys ₹180 an hour. Job takes 50 hours. That’s ₹9,000.

Anjali: What about machine time?

Vikram: Machine runs when the guy’s working, no?

Anjali: Not always. And machine costs money even when nobody’s touching it.

This is the second place money hides.

For her bracket job, Anjali tracks:

- CNC operator: 18 hours × ₹180/hour = ₹3,240

- Helper: 18 hours × ₹120/hour = ₹2,160

- CNC machine time: 18 hours × ₹850/hour = ₹15,300

- Setup time (separate): 3 hours × ₹950/hour = ₹2,850

- Finishing/inspection: 8 hours × ₹150/hour = ₹1,200

- Consumables: Electricity, coolant, tooling wear = ₹3,250

- Total labor + machine: ₹28,000

Vikram: ₹850 per hour for the machine? How do you even calculate that?

Anjali: Machine cost me ₹45 lakhs. Life is 10 years. That’s ₹4.5 lakhs depreciation per year. Add maintenance, repairs, insurance. Comes to ₹6.2 lakhs annually. Machine runs 2,000 hours a year. That’s ₹310 per hour just for depreciation and maintenance.

Then add power. CNC pulls 15 kW. That’s ₹120 per hour. Coolant, tooling wear, calibration, another ₹420 per hour. But that’s precision automotive work.

Vikram: That seems high.

Anjali: Does seem high. But we do precision automotive parts. Carbide inserts cost ₹2,500 each, last 40 hours. That’s ₹62/hour just for cutting tools. Add coolant, calibration, fixtures, ₹420 is reality for precision work.

Your sheet metal work? Probably ₹150-200/hour consumables. Adjust the formula to your industry.

Total: Depreciation (₹310) + Power (₹120) + Your consumables (₹150-200) = ₹580-630/hour for sheet metal. Not ₹850.

Vikram: So the number changes by industry.

Anjali: Exactly. The formula stays the same. The inputs are yours.

Vikram: You mentioned setup separately?

Anjali: Setup used to disappear into my averages. Small batches were killing me.

Setup is time spent preparing machines, loading tools, running test pieces. On small batches, it’s massive.

Example: 100-unit batch might need 4 hours setup + 6 hours run time = 10 hours total.

If you only count run time (6 hours), your cost per unit is wrong. Setup eats 40% of total time on small batches.

Anjali: I track setup separately now. Changed everything.

Number Three: Overhead Allocation (Where Most People Screw Up)

Vikram: Overhead is just… rent and office stuff, right?

Anjali: Rent, yes. But also admin salaries, utilities, insurance, maintenance, accounting, quality control. Everything that’s not direct material or labor.

Vikram: How do you split that across jobs?

Anjali: That’s the ₹10 lakh question.

Here’s where most manufacturers lose money silently.

Anjali’s monthly overheads: ₹4.8 lakhs

- Rent: ₹1.2L

- Admin salaries: ₹1.5L

- Utilities: ₹85K

- Maintenance: ₹60K

- Insurance, accounting, misc: ₹55K

Her machine runs 320 productive hours per month.

Overhead rate = ₹4.8L ÷ 320 hours = ₹1,500 per hour

For her 18-hour bracket job: 18 × ₹1,500 = ₹27,000 overhead allocation.

But she doesn’t use ₹27,000.

Anjali: Complex jobs eat more overhead than simple ones. Small batches need more setup, more QC, more planning.

Anjali figured out: ‘I was winning all the complex custom jobs and losing money. Losing the simple repeat jobs even though they were profitable. I had it backwards. Complexity-based overhead allocation fixed this.’

Result: You overprice simple work (lose bids). Underprice complex work (lose money).

Anjali’s adjustment:

She allocates 60% of overhead to complex/custom jobs. 40% to simple/repeat jobs.

For her bracket job (custom, moderate complexity):

- Base allocation: ₹27,000

- Complexity adjustment: 60% = ₹16,200

- Overhead for this job: ₹15,600 (she rounded)

Vikram: That seems… complicated.

Anjali: It’s just two numbers. Simple jobs get lower overhead rate. Complex jobs get higher. Takes me 5 minutes per quote now.

Before I did this, I was winning all the complex jobs and losing money. I was losing the simple jobs and they were profitable. I had it backwards.

Number Four: Profit Margin (The Only Part That’s Actually Yours)

Now Anjali has:

- Material: ₹45,000

- Labor + Machine: ₹28,000

- Overhead: ₹15,600

- Total cost: ₹88,600

Anjali: This is my cost. Everything before this is just covering expenses.

She adds 25% margin: ₹22,150

Final quote: ₹1,10,750

Vikram: You’re adding 25% on top of everything?

Anjali: Not on material. On total cost. I used to add 40-50% on just material. Thought I was making great margins.

Then I calculated the actual costs. I realized my ‘profit’ was paying for labor, overheads, and scrap. Real profit was maybe 8-10%.

Now I know my costs. I add 20-30% on total cost. Win more bids. Make more actual profit.

Industry data supports this: Manufacturers with accurate costing systems improve margins 15-20% within 6 months, not by raising prices, but by knowing which jobs to take and which to walk away from.

We’re SoftwareHunt. We work with manufacturing owners running on Tally, Excel, and lean teams to understand your operational leaks and growth challenges. Our team is happy to connect with you, understand your personal pain points, operational leaks and growth challenges and go beyond platform listings/information to help find the right solution for you.

We’ll help you translate symptoms into clear financial insight and show you where to focus first – at no cost to you.

To email an advisor for a quick fit-check write to us at connect@softwarehunt.com

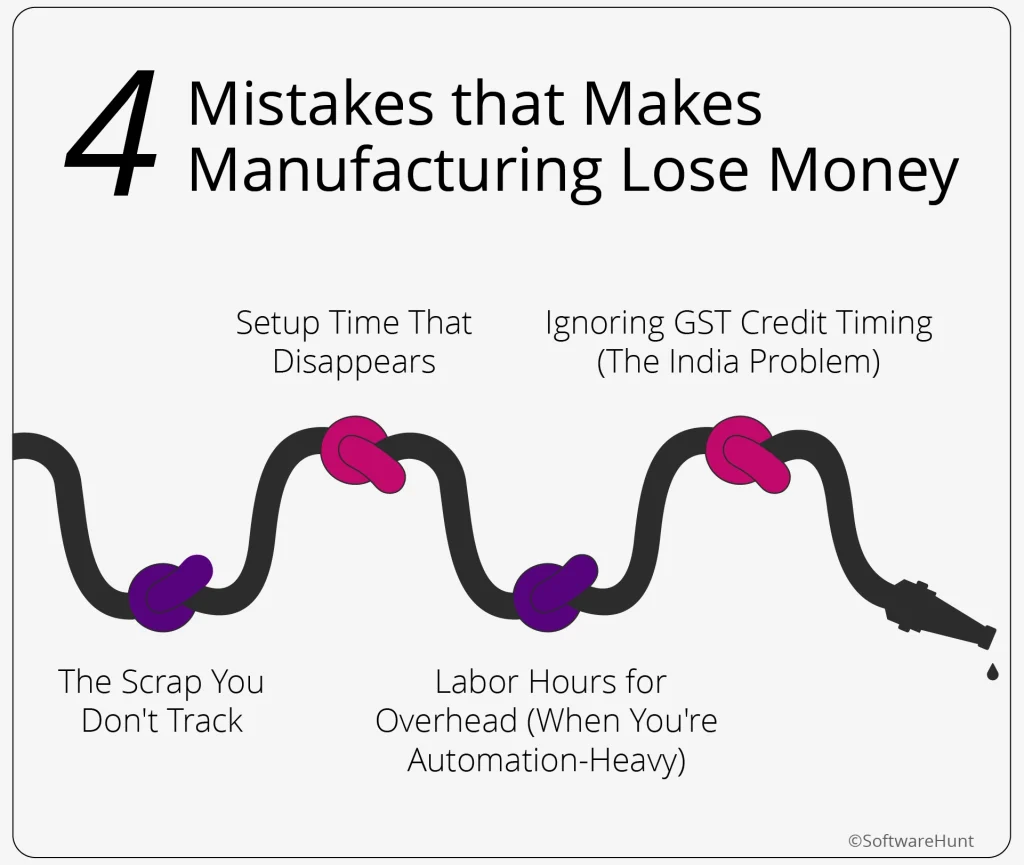

4 Mistakes that Make Manufacturers Lose Money

Vikram: Okay. So where did my ₹82K disappear?

Anjali: Let me guess. You ignored scrap. Didn’t track setup separately. Used some random overhead rate. And thought 60% markup covered everything.

Vikram: [Nods]

Anjali: Same mistakes I made. Let me show you where money hides.

Mistake One: The Scrap You Don’t Track

Vikram assumed: 5% scrap on his steel order.

Reality: His process generates 18-22% scrap. He’s never measured it.

On ₹3.25L material, that’s ₹40,625-55,250 unaccounted cost.

Fix:

Pick 10 recent jobs. For each:

- Weight/quantity of raw material purchased

- Weight/quantity of finished products shipped

- Calculate: (Purchased – Shipped) ÷ Purchased = Scrap %

Vikram: That’s it?

Anjali: That’s it. Takes 30 minutes. Use actual scrap rate in quotes, not guessed 5%.

Mistake Two: Setup Time That Disappears

Vikram: I quoted based on run time. 50 hours of actual production.

Anjali: What about machine setup? Tool changes? First-piece inspection?

Vikram: Maybe… 8-10 hours? I didn’t count it separately.

On a 50-hour job, 10 hours of uncounted setup is 20% missing cost.

Setup includes:

- Loading tools and fixtures

- Programming CNC

- Running test pieces

- Adjusting tolerances

- First-article inspection

Small batches get destroyed by this. A 100-unit batch might be 40% setup time, 60% run time.

If you only count run time, small batches look profitable. They’re not.

Anjali: I started tracking the setup separately 8 months ago. Discovered small custom jobs were losing ₹15-25K each. Nobody knew.

Mistake Three: Labor Hours for Overhead (When You’re Automation-Heavy)

Vikram: I allocate overhead based on labor hours. More labor = more overhead.

Anjali: Your CNC runs 10 hours a day with 2 hours of labor supervision?

Vikram: Yeah. Mostly automated.

Anjali: Then labor-based allocation is wrong. Machine time drives your overhead, not labor time.

Example:

Job A: Automated CNC job

- 2 labor hours, 10 machine hours

Job B: Manual assembly job

- 10 labor hours, 2 machine hours

If you allocate overhead by labor hours:

- Job A gets 2 units of overhead

- Job B gets 10 units of overhead

But your facility costs are driven by machines running:

- Electricity, maintenance, depreciation, floor space, all tied to machine time

- Job A should get 10 units of overhead

- Job B should get 2 units

Labor-based allocation undercharges automated work. Overcharges manual work.

Research shows this is a critical error in automated facilities: Overhead allocation must match cost drivers.

Anjali: Switched to machine-hour allocation 6 months ago. Some products became 15% more expensive, some 12% cheaper. Suddenly my margins made sense.

Mistake Four: Ignoring GST Credit Timing (The India Problem)

Anjali: One more thing. GST.

Vikram: I charge GST on the invoice. Client pays.

Anjali: But your material has GST too. And that credit doesn’t come instantly.

This is India-specific and hidden.

Example:

- Material purchase: ₹100 + ₹18 GST = ₹118 total outflow

- GST credit: ₹18 (eventually recoverable via GSTR-2B)

- Timing gap: 30-60 days

For monthly material purchases of ₹50 lakhs:

- GST outflow: ₹9 lakhs

- Credit delay: 30-45 days

- Cash flow impact: ₹9L tied up for a month

This doesn’t change your cost on paper. But it changes cash availability.

If you’re quoting tight margins and waiting 60 days for GST credit while paying vendors in 15 days, cash flow chokes.

Anjali: Took me 6 months to realize my ‘profit’ was just timing. Cash was always tight. Now I factor GST timing into payment terms.

Is This Method For You? Answer These Questions To Confirm.

Question 1: How many different jobs do you do monthly, more than 15, or mostly the same repeats?

Question 2: When you discover a job lost money, how long after delivery do you find out – days, weeks, or months?

Question 3: Is your monthly overhead (rent, admin, utilities, salaries) more than 20% of your monthly material cost?

Question 4: How often do you update job costs, daily, weekly, or monthly? Can you catch material price changes fast enough?

Question 5: Would you spend 40 hours (10 per week for 4 weeks) to improve margins 15-20% over 6 months?

If yes, this method works for you. If no, you’re choosing guessing over knowing.

If you answered YES to 3+ questions, proceed to the 4-week plan.

How to Actually Start

Vikram: Okay. I’m sure. What should I do first on Monday morning?

Anjali: Four weeks. One step every week.

Week 1: Find out how much material you waste.

Job: Find out the actual scrap rate (30 minutes)

Steps:

Choose 10 jobs that have been finished recently.

For each, write down:

Weight and quantity of raw materials bought

Finished goods sent (weight/quantity)

Do the math: (Purchased – Shipped) ÷ Bought = % of waste

Average of 10 jobs

For example:

- Job 1: Bought 1,000 kg, shipped 850 kg, and 15% of it was wasted.

- Job 2: Bought 500 kg and shipped 465 kg, which is 7% waste.

- Job 3: Bought 1,200 kg, sent 960 kg, and lost 20% of it.

Average: about 14% waste

Vikram: What then?

Anjali: Put 14% in the quotes for next month. Not guessed 5%.

Week 2–3: Keep track of machine and labor hours

Task: Keep track of the time for 10 jobs (actual tracking)

Steps:

Choose ten jobs that are currently available, some of which are easy and some of which are hard.

For each, put a time stamp:

Start setup to Finish setup

Start of production to End of production

Starting to finish to Finishing done

Note: Who worked and what machine was used

Figure out: Ratio of setup time to run time

Pattern you’ll notice:

Small batches: 40–50% of the time is spent setting up

10–15% of the time is spent setting up large batches.

Difficult tasks: More time for finishing and checking

Anjali: This showed me that small custom orders were taking 6 hours to set up and 8 hours to make. I was charging for a total of 8 hours. The truth was 14 hours.

Week 4: Find out how much your overhead costs.

Monthly overhead divided by productive hours (20 minutes)

Steps:

List all costs that are not linked to specific jobs:

Rent: ₹X

Salaries for admins: ₹Y

Utilities: ₹Z

₹A for maintenance, insurance, and accounting

Monthly overhead: ₹M

Last month, there were H hours of productive machine time.

Don’t add up time spent on maintenance, downtime, or being idle.

Only real production hours Count: Overhead rate = M ÷ H = ₹R per hour

Example (Anjali’s numbers):

₹4.8L in monthly overhead; 320 productive machine hours

₹1,500 per hour for overhead

To figure out how much overhead to charge each job, multiply ₹1,500 by the number of hours worked.

Vikram: Did you hire anyone to help with this?

Anjali: My CA helped with overhead rate calculation, took him 45 minutes, charged ₹2,500. Worth it because I would’ve screwed up the formula. Rest I did myself.

Vikram: Should I buy costing software for this?

Anjali: Not yet. Excel is fine for 4-number framework. Software helps when you’re doing 50+ quotes monthly with complex BOMs. You’re at 15-20 quotes monthly? Excel + discipline works. I switched to software after 18 months when quoting time became the bottleneck, not accuracy.

Vikram: What’s the threshold?

Anjali: If you’re quoting 50+ jobs monthly and losing time entering the same data repeatedly, software saves 10 hours weekly. That’s worth ₹30K/month software cost.

If you’re at 15-20 quotes monthly? Your time bottleneck is thinking, not data entry. Excel is sufficient.

Vikram: [Nods] And the cost?

Anjali: ₹500-2,000/month for decent costing software. But you’d waste ₹15K buying it before you need it. Master Excel first. Migrate to software if you hit 50+ quotes monthly.

Start Using Real Numbers After One Month

Anjali: After four weeks, you’ll have: The real waste rate (not a guess of 5%)

Actual time needs (setup time is different from run time)

The real overhead rate, not a random markup

Quotes for building:

The cost of materials is the cost of the raw materials plus the cost of shipping and handling. The cost of labor and machines is the cost of labor hours times the labor rate plus the cost of machine hours times the machine rate plus the time it takes to set up.

Overhead = Job hours × Overhead rate

Total cost = Material + Labor + Machine + Overhead. Quote = Total cost + (Profit margin % × Total cost)

Vikram: The first month seems slow. Automatic for the second month?

Anjali: Exactly. You’re setting it up in the first month. It’s 30 minutes a week in the second month.

What It Looks Like When It Works

Two empty chai cups sit on the table.

Evening factory sirens mark shift change.

Workers stream toward parking lots – scooters, bikes, shared autos.

Vikram walks back to his unit. Excel sheet still open on his phone.

But something’s different.

That ₹82,000 loss doesn’t feel like bad luck anymore.

It feels like data. Like a question: What did I actually miss?

Next quote won’t be material + 60%. It’ll be:

- Material (including 14% measured wastage)

- Labor + machine (including 8 hours setup)

- Overhead (at ₹1,200/hour based on actual calculation)

- 25% profit margin on total cost

Not a guess. Math.

Anjali’s voice echoes:

Costing isn’t magical. It’s just honesty about your actual costs. Everything after that is profit or loss. Your choice which one.

Vikram opens a new Excel tab.

Title: Week 1 – Material Wastage Calculation

He starts typing.

Ending Thoughts

Manufacturing cost estimation isn’t about perfection. It’s about knowing four numbers better than you do today: material (with real scrap), labor plus machine time (with setup separate), overhead (allocated properly), and profit (on total cost, not just material). Get those four right, and the ₹82,000 losses stop. You won’t win every bid. But you’ll know why you lost, and that’s worth more than guessing your way to bankruptcy.

Core principle: If you don’t measure it, you can’t manage it. If you can’t manage it, you’re just hoping.

We’re SoftwareHunt. We work with manufacturing owners running on Excel, Tally, and tight cash flows. Our advisors help you identify operational leaks like hidden setup costs and overhead allocation errors and translate symptoms into clear financial decisions. We show you where to focus first, at no cost to you.

Email us: connect@softwarehunt.com